Business Articles - Employees

Articles & Tips

Every year, a notice comes in the mail from our insurance carrier informing us that we're due for an audit of our workers' compensation exposure. If you've been through one of these, you know that it's either a relative breeze or a royal pain, depending on your level of preparedness. We've always had our paperwork more or less in order, but, over the years, we've learned specific ways to minimize the time and money spent on this business essential.

The most important thing you can do to save yourself money at an audit is to be completely prepared: Have your payroll records and all subcontractor certificates ready for review. It may also help to put the auditor at ease if you provide a little hospitality in the form of coffee and a cookie or muffin. If you're nice to him or her, the favor's likely to be returned.

Choosing a Carrier

Shopping for workers' compensation insurance isn't entirely a matter of getting the best price. Because it's a state-regulated service, the basic rates are set in stone. Individual insurers are allowed to apply a markup, however, which varies by carrier. These markups are a matter of public information, available on request from your state regulatory agency. The differences are generally minor, 1 or 2 percentage points (but may be as much as 15% for certain classes in some states).

What I look at is the quality of the service provided by the agent and the carrier -- how helpful are they in providing information and explaining options? You may find that one agency seems more evenhanded assessing your classifications than another. Some understand the construction industry, and others do not. Look for an agent who takes the time to discover what you do and how you do it. In the long run, the right vendor can save you significant amounts of money by advising you how best to put your insurance program together, rather than merely comparing rates and letting mistakes from one year carry over into another.

Use the Right Classifications

To control your annual expenditure, make sure to classify your employees correctly. It's a big mistake to post all your employees under a single classification; a carpenter carries a much higher exposure rating than an office employee. In most, but not all, states, insurance carriers determine the experience ratings of an industry based on the Scopes Manual, published by the independent National Council on Compensation Insurance (NCCI). Your state or carrier may even allow you to split the payroll of an individual employee between classes. The NCCI rules state that to split the payroll of an employee between classes, you must keep a daily payroll record of the different classifications -- you can't use broad percentages. Work with a knowledgeable insurance professional to be sure you're taking advantage of all rules and regulations in the best way possible.

Who's who? Never leave classification entirely up to the carrier. Your insurer (or auditor) is likely to take the simplest route to classification -- if they're covering Robert's Remodeling, for example, every employee, including Robert's accountant, salesperson, and receptionist, may be automatically classified under general carpentry. Ask your insurance agent to walk you through the various classifications and find the right categories for your people. The difference can be huge: I pay $11 per $100 on a carpenter's salary, but only 30¢ per $100 on a salesperson. Everyone from field supervisors to the sales and clerical staff must be properly classified (see Figure 1).

| Sample Classifications and Rates | ||

| Scopes Classification |

Job Category

|

Rate per $100 |

| 5651 | Carpentry, apartment, 3 stories or less | |

| 5437 | Carpentry, interior |

$ 5.58 |

| 5645 | Carpentry, single-family | $10.39 |

| 5478 | Carpet installation | $ 4.07 |

| 5348 | Ceramic tile | $ 6.48 |

| 5610 | Cleaning/debris removal | $ 2.53 |

| 5445 | Drywall | $ 5.56 |

| 5474 | Painting | $ 7.00 |

| 5551 | Roofing | $15.72 |

|

Rates for Yorktown, Va., 2002.

|

||

Figure 1. The differences in rates from one trade

to another are sizable. That's why it's important to classify each job and worker

individually. It may be worthwhile to split employees between classifications

if you keep good records and your state and insurance carrier allow it.

As the business owner, I classify myself as a salesperson. Why don't I take

myself off workers' comp and just carry a disability policy instead? Because

under the sales classification, I pay next to nothing -- certainly less than

the cost of a disability policy. (Nonetheless, I also carry a disability policy

because it covers me if I'm injured away from the job or become seriously ill,

which workers' comp doesn't cover.)

Primary functions. Years ago, we broke down

our employee classifications by percentage of exposure -- if an employee spent

40% of the year roofing and 60% of the year painting, we'd report that, and

our insurer adjusted the rates. That worked for a couple of years, but eventually,

our insurer disallowed mixed classifications and arbitrarily reclassified my

entire company under general carpentry.

That was my wake-up call. Determined to classify each of my employees properly,

I contacted my state's insurance regulatory bureau and requested a list of possible

classifications within a residential remodeling business. The bureau sent excerpts

from the Scopes Manual, and I compared my employees' functions against

them. Then I contacted the NCCI to get the payroll rates for our area per $100

for the respective classifications.

Classifying an employee under an inappropriate category is illegal, but to classify

a worker who performs a range of tasks under his or her primary capacity is

generally accepted. For example, an employee who is primarily a carpenter may

install a minor amount of roofing without being forced into the costly roofing

classification. And, as a salesperson, I can take a fall from a roof during

a sales inspection and still have my injuries and downtime legitimately covered

by workers' comp. But if an employee installs roofing 60% of the time, roofing

is the appropriate classification for that person. We subcontract all of our

roofing for that reason.

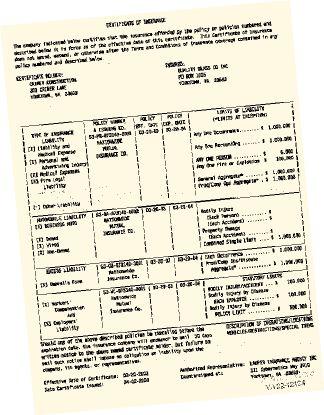

Check Those Certificates of Insurance

Any subcontractor or trade contractor who works for us has to provide us with

a current (annual) Certificate of Insurance -- one that covers the dates they're

actually working for us. At first, we dutifully collected certificates but didn't

really look them over. There are two boxes on a standard Certificate of Insurance,

one for Workers' Compensation, the other for Employers' Liability (Figure 2).

Figure 2. When you get

a Certificate of Insurance from a subcontractor, make sure the box next to Workers'

Compensation is filled in. Otherwise, you may become liable for paying that

sub's comp premiums. Aggregate coverage should be at least $500,000 per incident.

We were caught with our pants down on that one. It turned out that the employer

liability certificates were meaningless to the workers' comp auditor. As a result,

we paid on every uninsured sub's invoice for services rendered to my company

during the past year. Although it cost us hundreds, not thousands, of dollars,

it was an entirely avoidable and unpleasant surprise. Make sure that the Workers'

Compensation box is checked and that the aggregate coverage is at least $500,000

per incident.

Make Sure Subs Itemize Labor

In one instance, we hired a solo roofer who couldn't provide a Certificate of

Insurance. The problem was, the bill he turned in wasn't itemized by labor and

materials; it was a lump sum invoice for $9,000. At the audit, we had no way

to substantiate that nearly half of the invoice reflected material costs. Auditors

don't argue, and they don't make judgment calls. If your records only show a

lump sum amount, you'll end up paying on that total. Now we always make sure

that our records and our subcontractor invoices itemize labor and materials.

After reviewing your subcontracted labor, the auditor will want to see your

941 quarterly payroll report, the form you use to pay your payroll tax. Because

I want to control my employee category selection, I supply the auditor with

a list that identifies each employee in his or her respective category. Individual

employee earning reports are a simple menu choice in our Peachtree accounting

program or can be taken directly from form 941.

Lowering Risk

Your insurance may be provided through your state's assigned-risk pool, which

means that your insurer considers your company a poor risk. To get out of that

pool, you first have to find out why you've been assigned to it. Your company

may simply perform the kind of high-risk work that triggers a high experience

rating. Maybe you should be hiring self-insured subcontractors to perform your

riskiest tasks, like roofing.

If your company shows a significant accident and claims rate, your rates are

likely to be higher the following year, and for years to come. A single $10,000

claim settlement is less likely to trigger a high rating than a half-dozen minor

incidents.

Prevention still the best cure. Look at your

company's past claims history and consider whether you've taken proper corrective

actions. Institute and maintain a company safety program. It may take a few

accident-free years to prove that your risk rating should be lowered again,

but it's certainly a worthwhile exercise. Showing proactive concern for your

employees' safety goes a long way toward eliminating lingering resentment if

an accident should occur. Remember, everyone looks good in safety glasses.

To File or Not to File

That may be a question you'll ask yourself when an employee suffers an apparently

minor injury. Rather than see your rates increase following a few stitches or

a broken bone, you might be tempted to cover the medical costs and recuperative

time out of pocket. Be careful. If you don't report the injury when it occurs

and complications from that same injury arise later, the carrier will decline

coverage. You may also be in violation of state law. Your company's assets could

then be left wide open to a costly lawsuit, bound to be far more expensive than

even a long-term rate hike.

By Robert Criner

This article has been provided by www.jlconline.com. JLC-Online is produced by the editors and publishers of The Journal of Light Construction, a monthly magazine serving residential and light-commercial builders, remodelers, designers, and other trade professionals.

Join our Network

Connect with customers looking to do your most profitable projects in the areas you like to work.